Trusts

People commonly think that if a plan is in trust, they lose access. this is usually not the case.

We have had several situations where clients have had Life insurance cover in Trust & this was extremely useful to them.

This meant:

They could access benefits from the State as funds belong to the trust not the client. this means they can “BORROW” from the trust when needed with no need to repay.

Funds were not taken to pay care fees. The trust owned the funds so it did not for part of the clients assets.

Less tax was applied to an estate on death. Again The trust owns the funds.

A divorce settlement of a child was protected. If you dont own it , it cant be take of you.

They are numerous reasons cover should be in trust.

CHECK YOUR COVER AND MAKE SURE YOU HAVE THE SIGNED TRUST FORM INS YOUR POSSESSION

Get in touch with ourselves (help@kgb.ie)or your existing Financial advisor to make sure you are properly protected.

MOST PEOPLE DONT KNOW ABOUT TRUSTS TO DO TELL YOUR FRIENDS

TRUST (LAW) The legal definition.

an arrangement whereby a person (a trustee) holds property as its nominal owner for the good of one or more beneficiaries.

“a trust was set up”

Questions & Answers to save you time

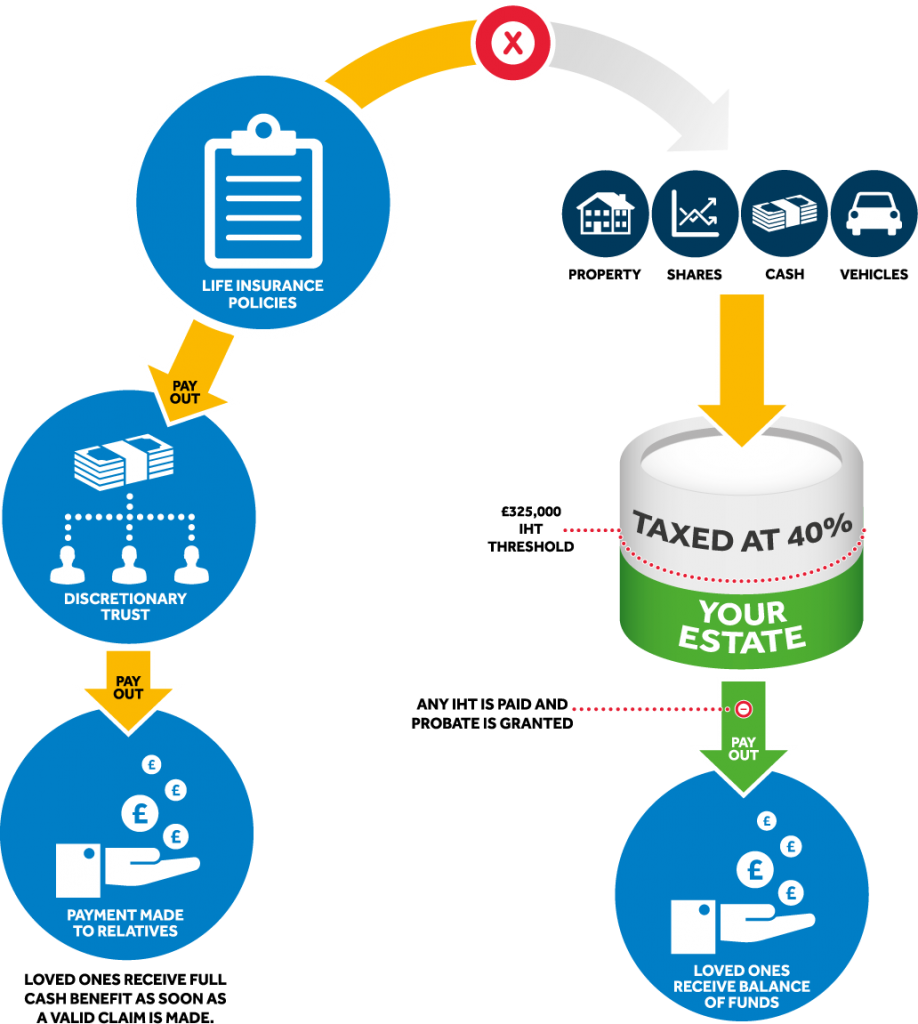

When the assets (life policies) have successfully been transferred into trust, they’re no longer subject to Inheritance Tax on your death. Others pay income and capital gains tax at higher rates. So it’s important to know what type of trust you have. The kind of trust you choose depends on what you want it to do.

In a trust, assets are held and managed by one person or people (the trustee) to benefit another person or people (the beneficiary). The person providing the assets is called the settlor. Different kinds of assets can be put in trust, including: cash/ property/ investments/life cover. We also have access to professional trust services for complex situations.

Control over your assets – if you don’t have a trust, your money might be used to pay off outstanding debts. Faster access to your money – without a trust, when you die your would-be beneficiaries would need to obtain probate, which can cause delays. Protect your beneficiaries from Inheritance Tax – writing life insurance in trust means the money paid out from your policy should not be considered part of your estate.

Putting your life insurance policies in trust is usually free of cost in our office.

Putting your house and assets into a trust costs and we will refer you to ProbateNI.com to discuss this further. They are particularly useful for protecting assets for vulnerable or financially naïve beneficiaries and can ensure that your hard-earned wealth is passed down through your own Bloodline, out of the clutches of ex in-laws and creditors.

Probateni.com is an external provider of trusts. K G Byrne & Associates Ltd are not providing advice through ProbateNI.com but merely an intorduction. Other providers may be available.

Creating a trust for life insurance:

One of the best methods to safeguard your family’s future in the event of your passing is to get life insurance in trust. Your life insurance policy is a valuable asset, and you can control how your beneficiaries receive their inheritance by placing your life insurance policy in a trust. Here, we go over the advantages of life insurance trusts as well as their operation, participants, and other factors.

What is a trust?

Trusts are a simple legal structure that allow you to leave assets to friends, family, or anyone else you want as your beneficiaries. Until the trust distributes funds to your beneficiaries, which can take a while, a trust is managed by one or more trustees, who may be family members, friends, or legal counsel.

How does putting life insurance in trust work?

You will need to decide which type of trust is right for you. Your options are:

- Discretionary Trusts – your trustees have a high level of discretion about which beneficiaries to pay when you’re no longer around, using your letter of wishes as a guide. Your letter of wishes outlines your intentions as to how trustees should administer the trust.

- A Flexible Trust – is a trust where there are two types of beneficiaries. The first type of beneficiary is the default beneficiary. These beneficiaries are entitled to any income from the trust as it arises. In practice, if the life policy is the only asset in the trust there will not be any income. The second type of beneficiary is the discretionary beneficiary. These discretionary beneficiaries only receive capital or income from the trust if the trustees make appointments to them during the trust period. If no appointments are made by the end of the trust period, the default beneficiaries will receive all the benefits.

- Survivor’s Discretionary Trust – this form of joint life insurance in trust pays out to the surviving policy owner; for example, if you die before your partner, they would be entitled to inherit your estate before your beneficiaries. If both policy owners die within 30 days of one another, your beneficiaries can benefit on the same basis as a Discretionary Trust.

- Absolute Trust – in this scenario, the beneficiaries are named individuals who cannot be changed in the future. This includes any children born later and a spouse following a divorce. The advantage of an Absolute Trust is that the pay-outs can be made quickly without long legal delays, and as with other trusts, the Inheritance Tax is likely to be nil or negligible.

Once your trust is set up, your trustees legally own the policy and must keep the trust deed safe – they can ask a solicitor to store the documents or find a safe place in their home. Your trustees will ultimately make a claim to your insurer when you pass away, so they will need the trust deed close to hand.

It’s worth remembering that as the settlor, you maintain responsibility for making sure your life insurance premiums are paid. It may be beneficial to hire a legal adviser to ensure the legal wording of your trust agreement is precise.

Who can be a beneficiary?

You can choose any person, or people, to be your beneficiaries – this will entitle them to receive a pay out in the event a valid claim is made. Contrary to what some people may assume, there are no rules that restrict who your life insurance beneficiary can be. For example, you could choose the following:

- A spouse or civil partner

- A child

- A relative

- A friend

- A charity

While you won’t be able to change your beneficiaries if you have an Absolute Trust, if you take out a Discretionary Trust, your trustees will have the freedom to decide who your beneficiaries are, and how much they’re entitled to receive from a pay out.

The benefits of writing life insurance in trust

There are many reasons why putting life insurance in trust is a popular option. Here are some of the ways you can benefit from a life insurance trust.

- Control over your assets – if you don’t have a trust, your money might be used to pay off outstanding debts. Putting life insurance in trust gives you greater discretion, as you can decide who to appoint as your beneficiaries and trustees. Setting up a trust is especially important if you’re not married or in a civil partnership, as otherwise, your assets may not transfer to the intended recipient.

- Faster access to your money – without a trust, when you die your would-be beneficiaries would need to obtain probate, which can cause delays. With a trust in place, your loved ones could receive the inheritance within a couple of weeks of the death certificate being issued.

- Protect your beneficiaries from Inheritance Tax – writing life insurance in trust means the money paid out from your policy should not be considered part of your estate. There are exceptions; for example, you may be liable for an Inheritance Tax charge on the value of the property on each ten-year anniversary. Currently, the standard Inheritance Tax rate is 40%, which is charged on the part of your estate above the £325,000 threshold.

How long does a trust last?

Technically, your trust can last up to 125 years – there is no expiry date for trusts set-up for charitable purposes – but ultimately, your trust agreement should last however long you deem necessary. Your personal circumstances may influence the length of time you stipulate; for example, the trust could last until a child grows up and marries.

Is there an extra cost?

There is no added cost to putting life insurance in trust. You can put your personal life insurance policy in trust when you take it out, or at any time after that – you simply need to own the policy. You should note that if you transfer your life insurance policy to another individual, this may have implications for your trust so it’s best to contact us directly or seek legal advice.